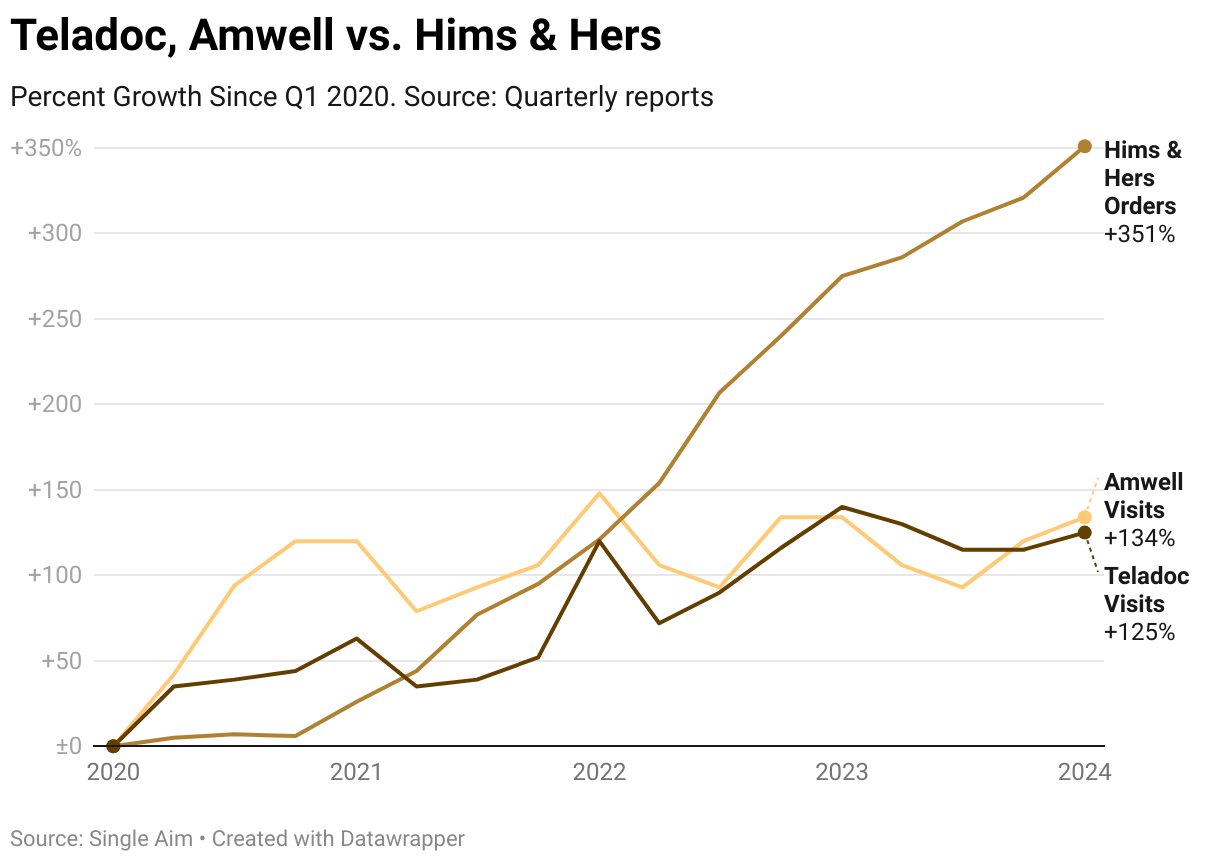

Is telemedicine dying? Is telemedicine thriving? A niche service before the pandemic, telemedicine experienced a dramatic demand surge in 2020, followed by settling to a new, much higher, baseline as life returned to normal. Since the peak of telemedicine venture funding in 2022, there has been a consistent stream of negative stories about telemedicine companies, shutdowns like Optum Virtual Care and Babylon, layoffs at companies like Workit and Calibrate, and Teladoc and Amwell stocks down over 90%. The health of telemedicine in 2024 is complex and seemingly contradictory.

Our report seeks to evaluate the relatively new telemedicine industry by comparing sub-verticals with enduring growth to those that were over-inflated by investors and to highlight untapped opportunities for growth, innovation and investment.

To provide a comprehensive analysis, we analyzed the LinkedIn work history of 115,077 clinicians who have ever worked at a telemedicine company. Given the service-heavy nature of telemedicine, we believe the number of employed clinicians scales with patient demand and provides a reliable point of comparison across companies and verticals.

Most data on telemedicine adoption focuses primarily on telehealth visits as a proportion of overall healthcare encounters, which, while important, doesn't fully capture the evolution and current state of the "Telemedicine Industry."

Our interest lies specifically in understanding the growth and development of the telemedicine industry, which is composed of "telemedicine jobs" within "telemedicine companies." These are roles and organizations that are almost exclusively dedicated to remotely delivered healthcare. This distinction is crucial, as it allows us to examine the ecosystem that has formed around telemedicine as a primary mode of care delivery, rather than just an occasional alternative to in-person visits.

We developed an index of 400 telemedicine companies that we used for this analysis. The index is made up of companies that employ over 2 clinicians with the majority reporting having fully remote jobs. Using LinkedIn employment data we were able to track the growth of these companies over time.

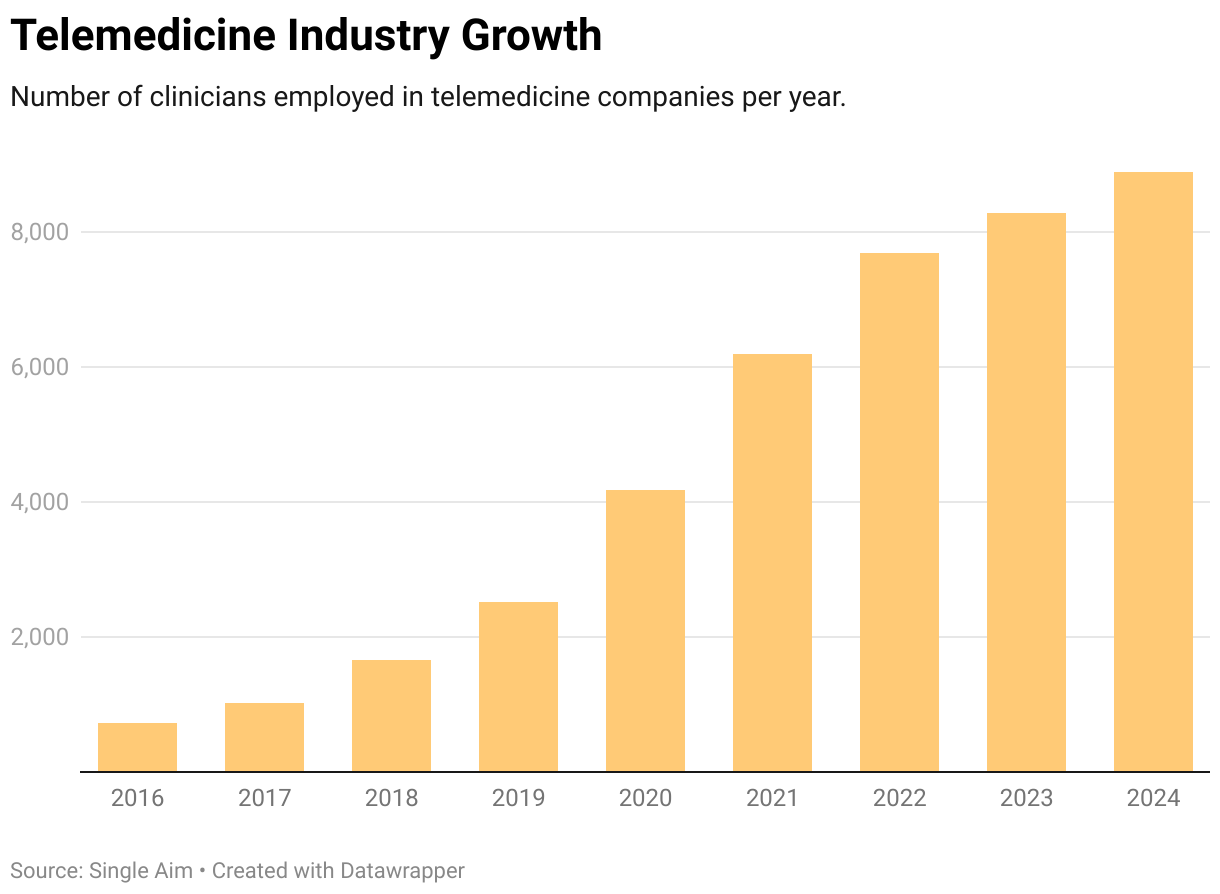

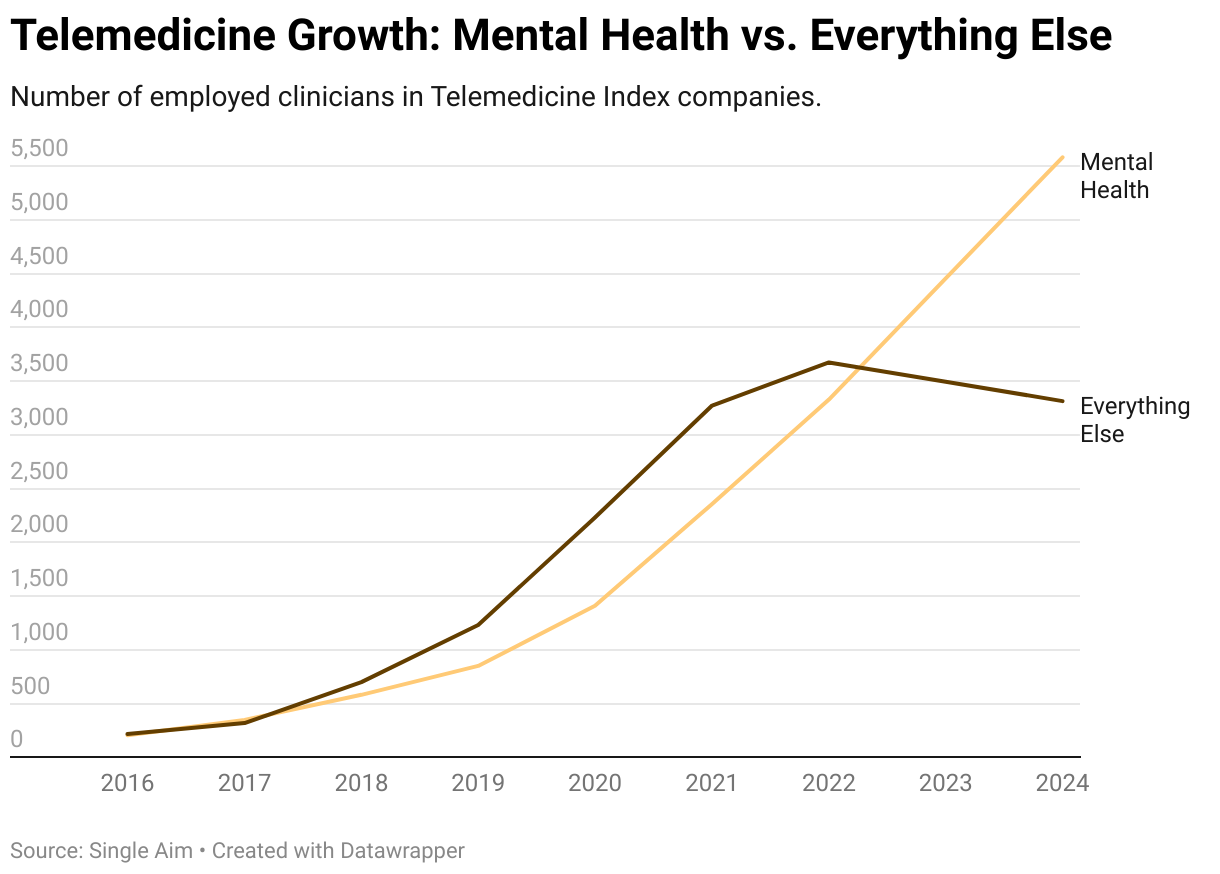

Overall telemedicine clinical employment has grown 1121% since 2016. The rest of this report will focus on looking beneath the surface of this chart, slicing and dicing the data, to understand what is growing, what isn’t, and why.

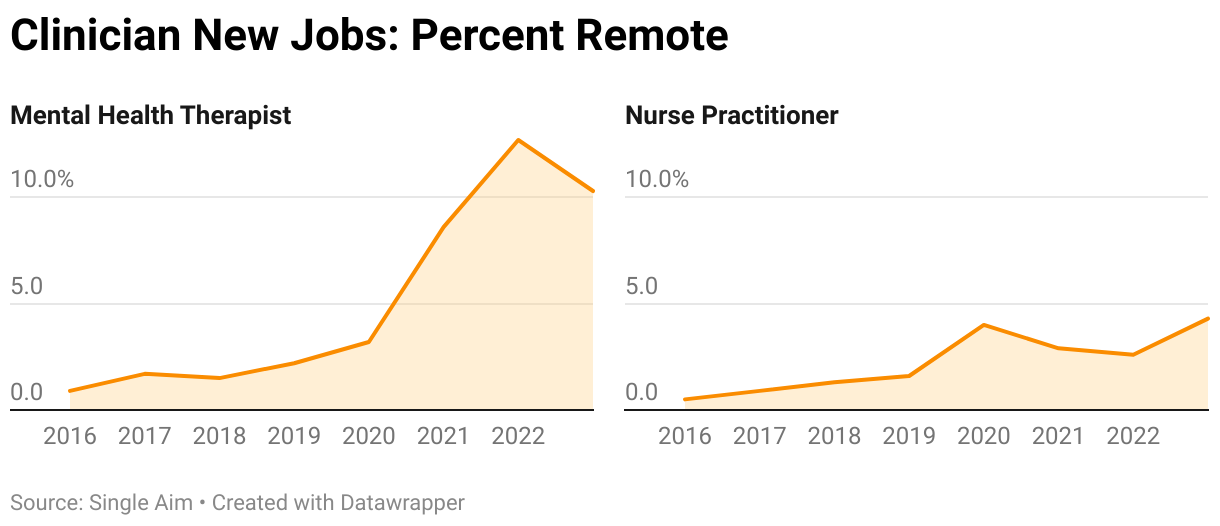

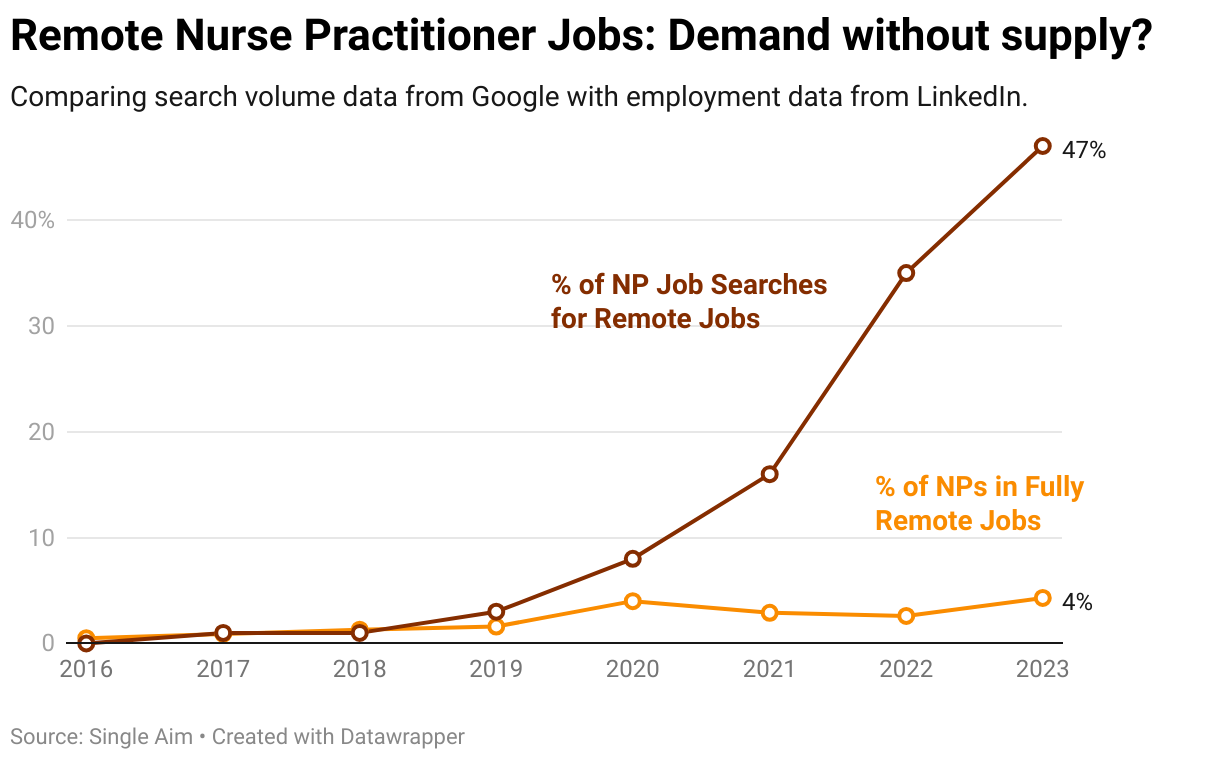

To understand the industry, we first need to understand who is working in it. Telemedicine jobs have experienced remarkable growth since 2020, with our data indicating this trend will continue. Based on our dataset, 4.3% of new nurse practitioner jobs and 10% of new mental health therapist positions are fully remote. These rates are 2.5x and 5x pre-pandemic baselines suggesting a sustained shift towards telemedicine.

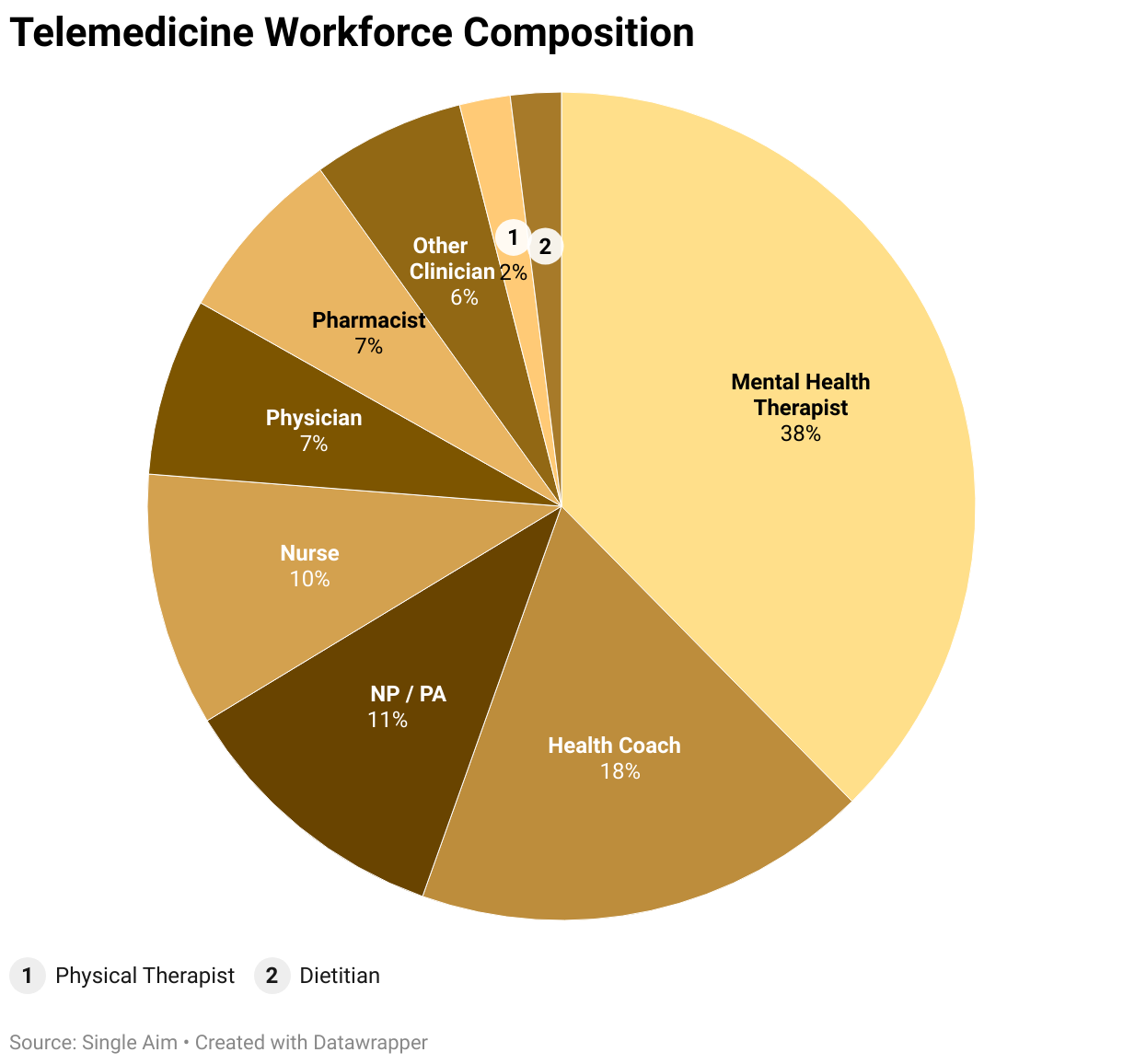

Mental health therapists dominate the telemedicine workforce at 39% of total clinicians, followed by health coaches (18%) and nurse practitioners/physician assistants (11%). Notably, over half of all telemedicine clinicians are either mental health professionals or work for mental health-focused companies, highlighting this specialty's particular affinity for remote delivery.

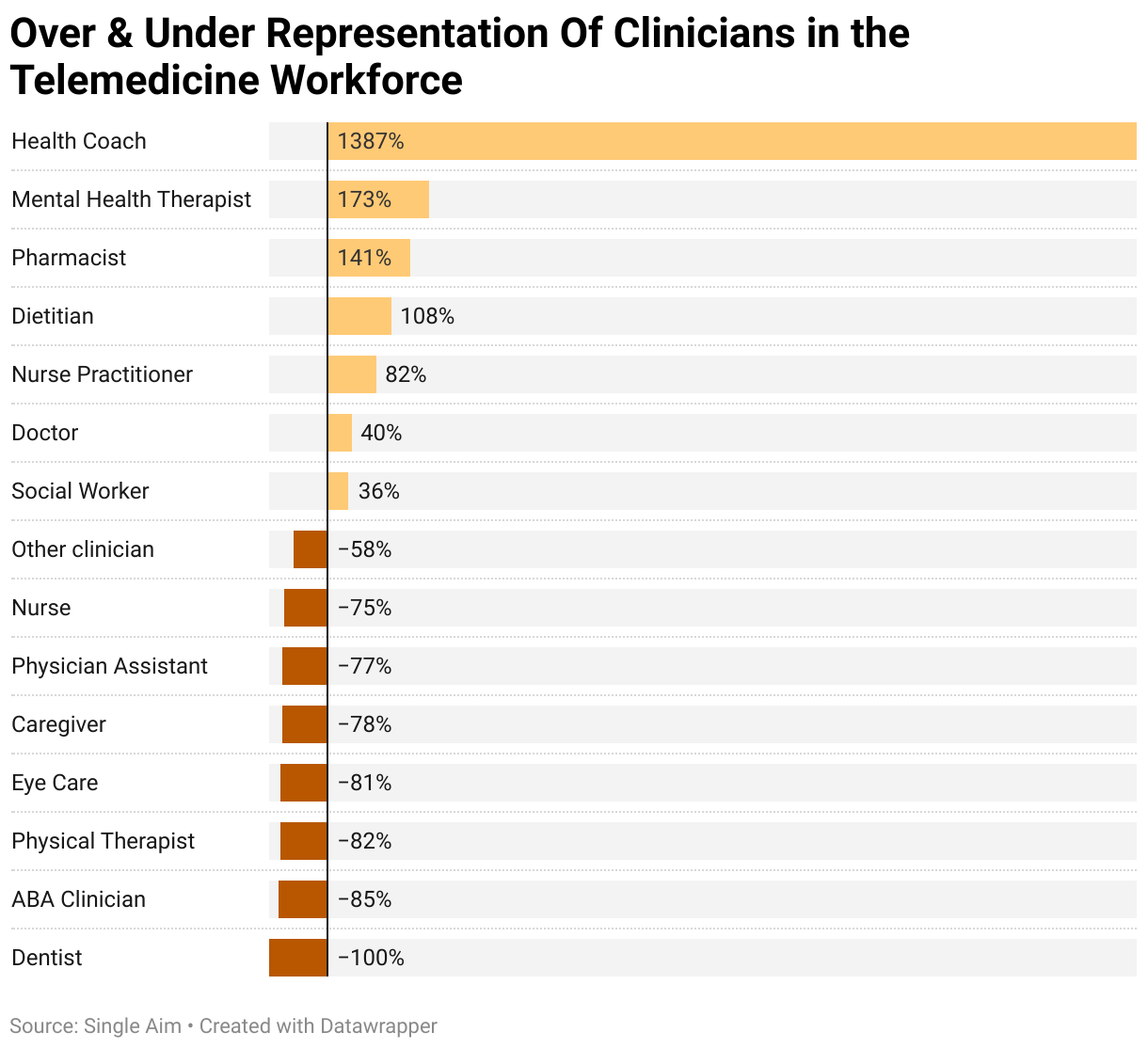

We looked at the representation of clinicians in the telemedicine workforce compared to the overall healthcare workforce. The same trends appear: mental health, nutrition, and pharmacy are highly over-represented within telemedicine, while fields requiring an in-person element like eye care, physical therapy, autism therapy, and dentistry are majorly underrepresented.

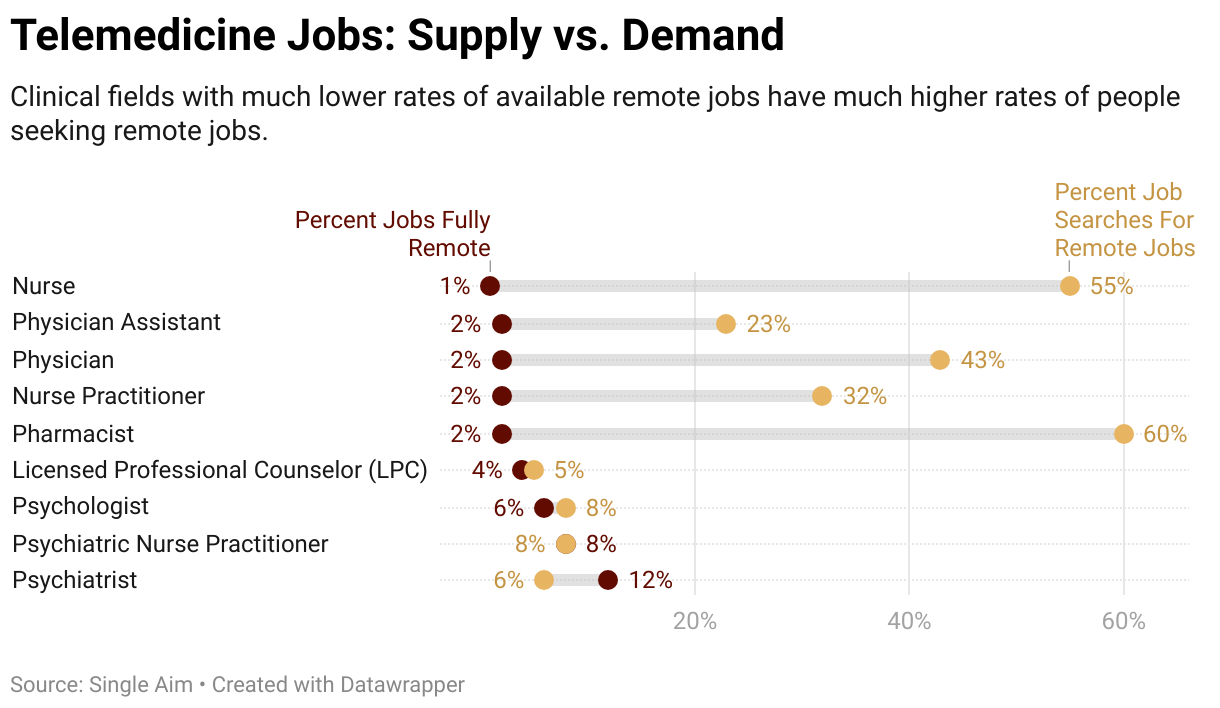

Our data reveals a significant mismatch between supply and demand for remote jobs in healthcare, particularly among medical professionals. While only 4% of new Nurse Practitioner (NP) jobs are fully remote, around 50% of NP job searches are for remote positions. This pattern extends to physicians, nurses, and pharmacists, indicating a substantial unmet demand for remote work in these fields.

In contrast, the mental health sector shows a balance between supply and demand. For mental health therapists, both the availability of remote jobs and the proportion of job searches for remote positions hover around 10%. This suggests a greater acceptance and expectation of remote work in mental health compared to other medical specialties.

Given that healthcare is often a clinician supply driven industry, this disparity highlights a growth opportunity for healthcare organizations to create or carve out more remote jobs. There are clinicians who want remote roles, but the jobs need to exist. We believe this will be a tailwind for continued creation and growth of niche telemedicine services that are able to be offered fully remotely.

Our analysis focused on companies primarily delivering healthcare services via telemedicine. Given the significant shift in the venture capital funding landscape in 2022, we sought to identify which companies and categories have demonstrated sustained growth versus those that may have been over-inflated by VC funding.

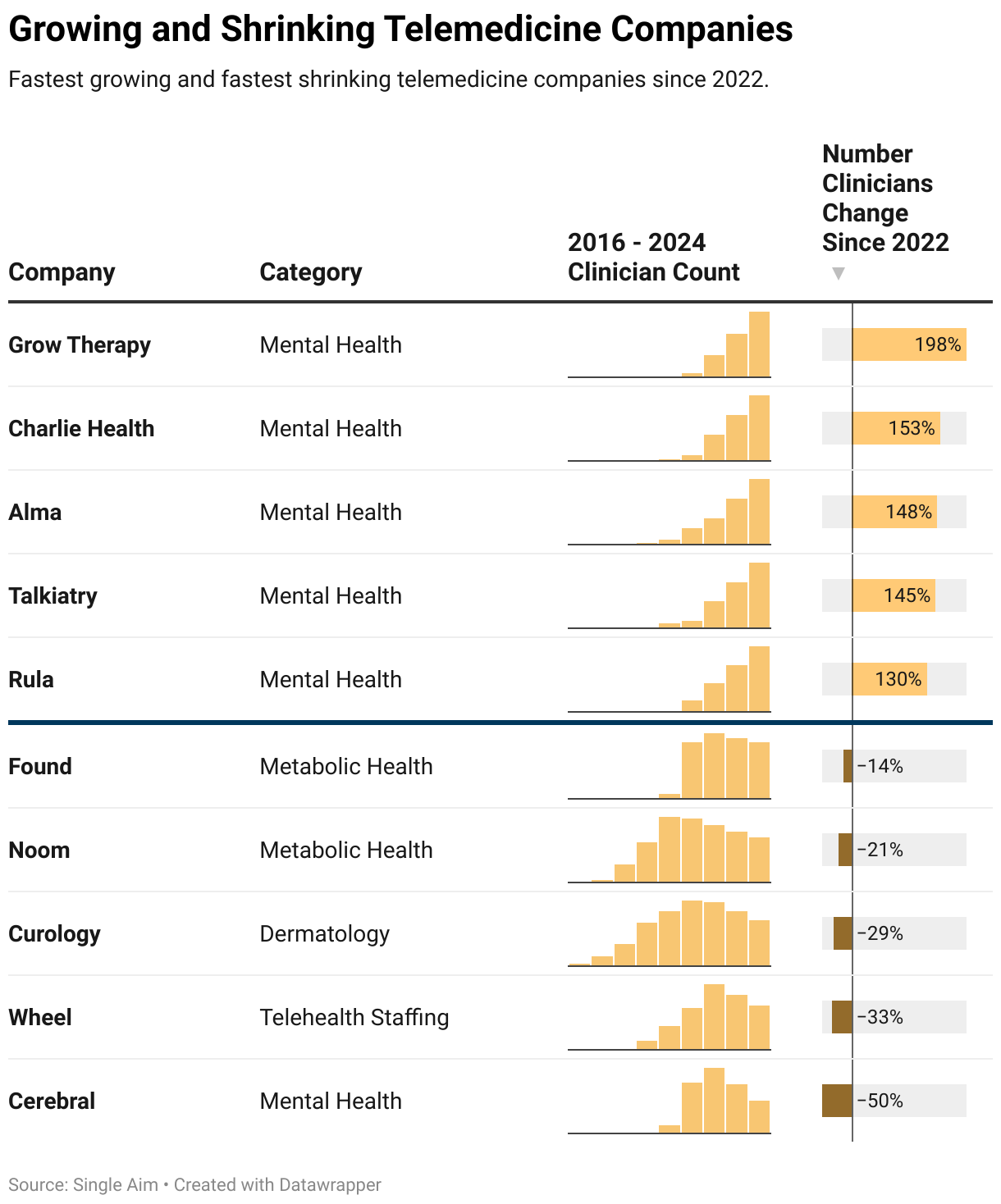

Examining specific company performance since 2022 reveals a clear trend: the largest fastest-growing companies are exclusively in the mental health sector. Conversely, companies that have experienced the most significant contractions are those primarily employing medical clinicians or operating in non-mental health fields.

In order to better understand these industry trends, we grouped companies by verticals and looked at their growth before and after 2022.

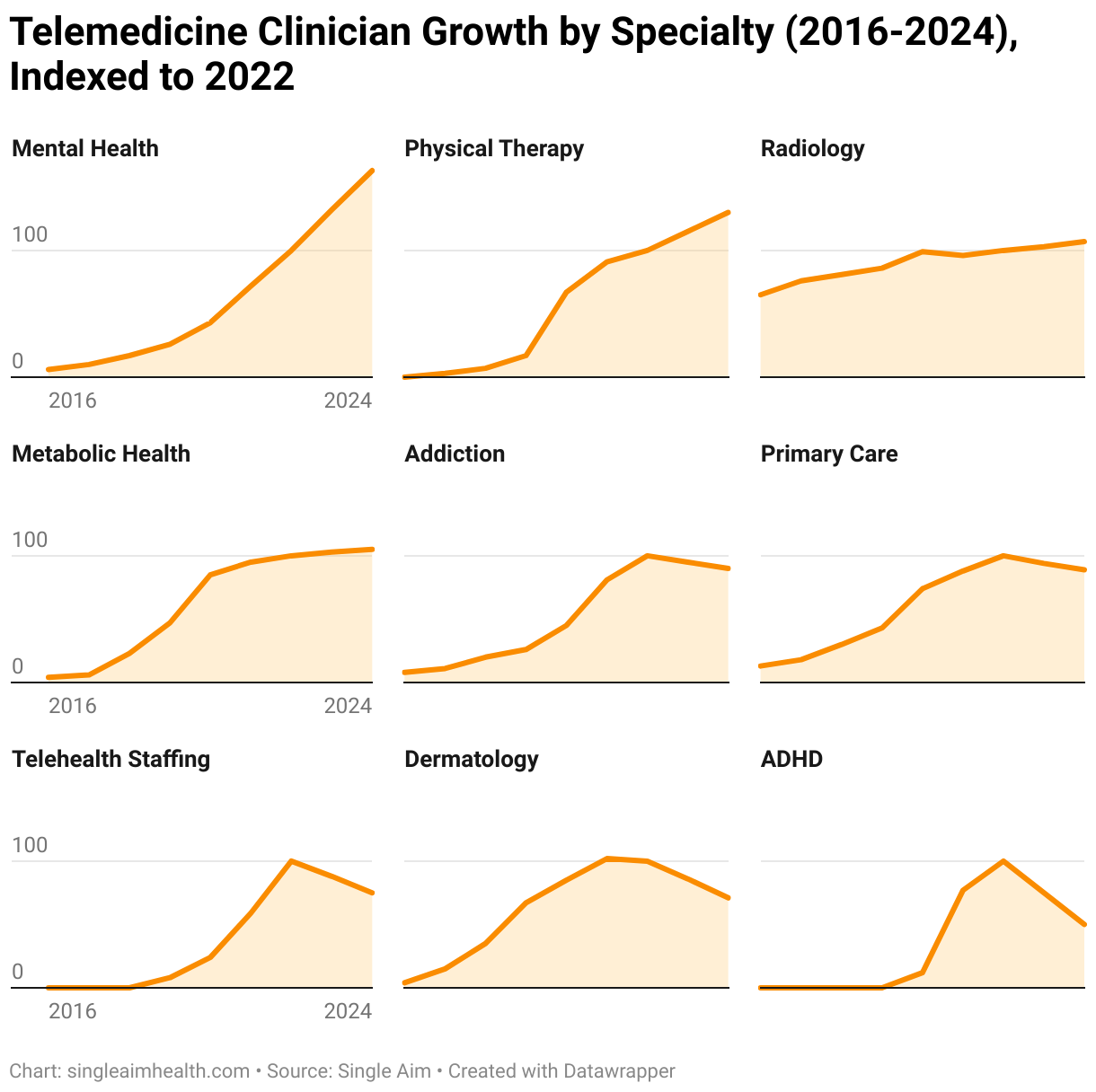

Mental Health, Physical Therapy, Radiology, and Metabolic Health are the four verticals that have grown since 2022. These four verticals appear to have different stories of growth.

Addiction, Primary Care, and Telehealth Staffing are all somewhat down since 2022. The shared story among these verticals is over-hiring during the VC boom times. After the initial pandemic surge, demand didn’t grow as fast as hoped, which led to some retraction. In these verticals, demand for telemedicine has not reduced, it just hasn’t grown as fast as hoped.

The category of companies that had significant business in online ADHD treatment, led by Cerebral, done., and Ahead, have experienced major retraction since 2022. Much has been reported about the troubles of these companies. Even after the retraction, our data shows Cerebral is still the largest employer of nurse practitioners, and the third largest employer of all clinicians within the telemedicine industry.

Now that we have a few years of growth data across many telemedicine companies, we can compare the relative growth of employment models and distribution strategies.

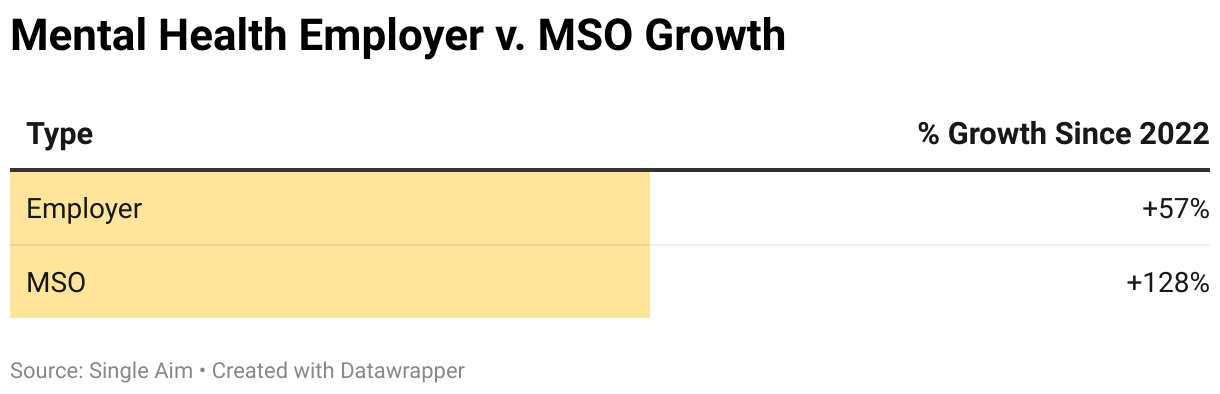

Most telemedicine companies follow an employment model hiring their clinicians as employees. More recently a handful of MSO or “business in a box” telemedicine companies have grown. The MSO companies usually contract with clinicians on a 1099 basis. These companies have been concentrated within mental health and include Headway, Alma, Sondermind, Grow Therapy, and Rula. To compare the models, we can look specifically at the mental health vertical.

Since 2022 both categories have grown, but MSO models have grown much faster increasing +132% in size. The MSO model has economic advantages for the company: clinicians bear the risk of their time being unutilized, and, in many cases, marketing is left up to the clinician. These are big advantages that allow MSO companies to scale faster.

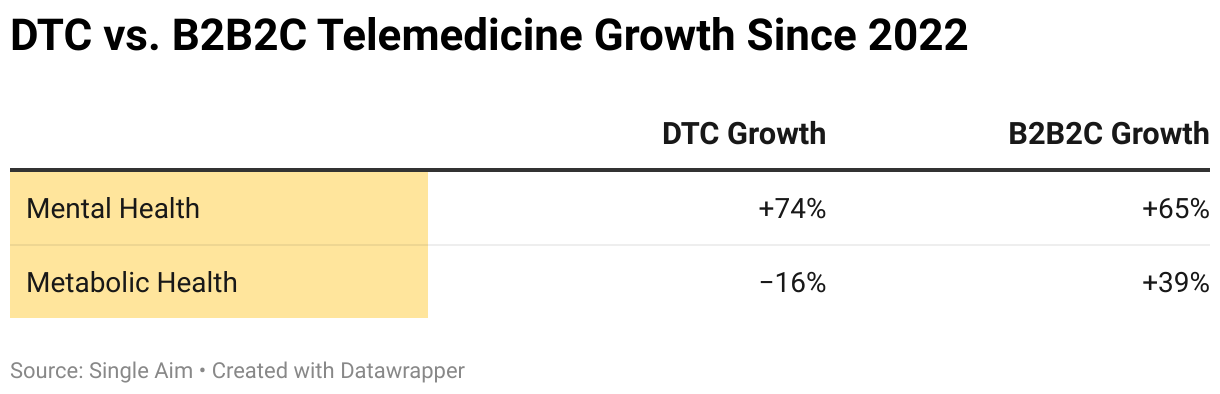

There are two primary ways for telemedicine companies to acquire new patients. The first is direct-to-consumer (DTC), in which they can market directly to them via consumer channels like Google, Meta, and Tiktok. The second is B2B2C, where the healthcare company gets access to non-public distribution channels via employers, payers, or other providers. So, which approach has shown enduring growth? Across all verticals DTC companies have shown +18% since 2022 while B2B2C has seen +39% growth. We can look specifically at Mental Health and Metabolic Health, which are two verticals with large amounts of both DTC and B2B2C companies.

Mental Health shows high growth in both models. This is driven by the set of mental health MSO companies which have been able to get wide payer coverage and acquire patients through broad DTC channels in addition to employer and health plan channels.

On the other hand, Metabolic Health shows stronger growth in B2B2C. B2B2C companies like Virta and Omada have shown consistent growth, while weight loss and GLP-1 focused DTC companies have been more boom and bust.

2020-2022 was a period of high scale experimentation fueled by venture funding in healthcare to understand what verticals and models were the best fits for telemedicine. Some experiments ended very poorly, some just ended, and others have emerged with sustained growth. After reviewing the growth of hundreds of telemedicine companies, let’s step back and synthesize some learnings.

Is telemedicine dying? Clearly not. Is telemedicine thriving? We would say so, though some verticals are still recovering from being given too much venture money. New wave telemedicine companies look more integrated into in-person care either by carving out remote jobs that fit into care teams or introducing technology that provides a novel "at-home" treatment experience. Standalone telemedicine services have shown to be an edge case in all of healthcare, so this is a natural evolution.

The telemedicine wave of 2020-2022 gave us answers to where telemedicine has enduring fit, but otherwise healthcare remains a primarily in-person and local industry. Our hope is the telemedicine wave, while not as immediately impactful as hoped, created a cohort of clinicians and operators game to build a next generation of healthcare services, likely grounded in in-person care, augmented by telemedicine, and utilizing efficiencies from technology wherever possible to provide better experiences for patients.

To inform this report, we analyzed the LinkedIn work history of 115,077 clinicians who have ever worked at a “telemedicine company”. Telemedicine Companies were defined as companies that employed at least 2 clinicians at some point between 2016 and 2024 and where the majority of those clinicians reported their jobs were fully remote.

There are limitations to this analysis. First, many clinicians don’t have LinkedIn profiles. Second, we only had access to public LinkedIn profiles. This means our numbers are an underestimate of the number of clinicians in the telemedicine workforce. The absolute numbers are not correct, but we believe since these limitations apply to all companies, comparisons across companies and across verticals should be accurate enough to extract insights.

Fair Use: Feel free to use this data and research with proper attribution linking to this study.

Media Inquiries: For media inquiries, contact team@singleaimhealth.com

Thanks to George Ribaroff, Kusum Chanrai, Tyler Olkowski, Lindsey Conon, Michael Ceballos, Jean Kim, Eddie Czech, Arpan Parikh, and Patrick Hurley for reviewing this article.

Is telemedicine dying? Is telemedicine thriving? A niche service before the pandemic, telemedicine experienced a dramatic demand surge in 2020, followed by settling to a new, much higher, baseline as life returned to normal. Since the peak of telemedicine venture funding in 2022, there has been a consistent stream of negative stories about telemedicine companies, shutdowns like Optum Virtual Care and Babylon, layoffs at companies like Workit and Calibrate, and Teladoc and Amwell stocks down over 90%. The health of telemedicine in 2024 is complex and seemingly contradictory.

Our report seeks to evaluate the relatively new telemedicine industry by comparing sub-verticals with enduring growth to those that were over-inflated by investors and to highlight untapped opportunities for growth, innovation and investment.

To provide a comprehensive analysis, we analyzed the LinkedIn work history of 115,077 clinicians who have ever worked at a telemedicine company. Given the service-heavy nature of telemedicine, we believe the number of employed clinicians scales with patient demand and provides a reliable point of comparison across companies and verticals.

Most data on telemedicine adoption focuses primarily on telehealth visits as a proportion of overall healthcare encounters, which, while important, doesn't fully capture the evolution and current state of the "Telemedicine Industry."

Our interest lies specifically in understanding the growth and development of the telemedicine industry, which is composed of "telemedicine jobs" within "telemedicine companies." These are roles and organizations that are almost exclusively dedicated to remotely delivered healthcare. This distinction is crucial, as it allows us to examine the ecosystem that has formed around telemedicine as a primary mode of care delivery, rather than just an occasional alternative to in-person visits.

We developed an index of 400 telemedicine companies that we used for this analysis. The index is made up of companies that employ over 2 clinicians with the majority reporting having fully remote jobs. Using LinkedIn employment data we were able to track the growth of these companies over time.

Overall telemedicine clinical employment has grown 1121% since 2016. The rest of this report will focus on looking beneath the surface of this chart, slicing and dicing the data, to understand what is growing, what isn’t, and why.

To understand the industry, we first need to understand who is working in it. Telemedicine jobs have experienced remarkable growth since 2020, with our data indicating this trend will continue. Based on our dataset, 4.3% of new nurse practitioner jobs and 10% of new mental health therapist positions are fully remote. These rates are 2.5x and 5x pre-pandemic baselines suggesting a sustained shift towards telemedicine.

Mental health therapists dominate the telemedicine workforce at 39% of total clinicians, followed by health coaches (18%) and nurse practitioners/physician assistants (11%). Notably, over half of all telemedicine clinicians are either mental health professionals or work for mental health-focused companies, highlighting this specialty's particular affinity for remote delivery.

We looked at the representation of clinicians in the telemedicine workforce compared to the overall healthcare workforce. The same trends appear: mental health, nutrition, and pharmacy are highly over-represented within telemedicine, while fields requiring an in-person element like eye care, physical therapy, autism therapy, and dentistry are majorly underrepresented.

Our data reveals a significant mismatch between supply and demand for remote jobs in healthcare, particularly among medical professionals. While only 4% of new Nurse Practitioner (NP) jobs are fully remote, around 50% of NP job searches are for remote positions. This pattern extends to physicians, nurses, and pharmacists, indicating a substantial unmet demand for remote work in these fields.

In contrast, the mental health sector shows a balance between supply and demand. For mental health therapists, both the availability of remote jobs and the proportion of job searches for remote positions hover around 10%. This suggests a greater acceptance and expectation of remote work in mental health compared to other medical specialties.

Given that healthcare is often a clinician supply driven industry, this disparity highlights a growth opportunity for healthcare organizations to create or carve out more remote jobs. There are clinicians who want remote roles, but the jobs need to exist. We believe this will be a tailwind for continued creation and growth of niche telemedicine services that are able to be offered fully remotely.

Our analysis focused on companies primarily delivering healthcare services via telemedicine. Given the significant shift in the venture capital funding landscape in 2022, we sought to identify which companies and categories have demonstrated sustained growth versus those that may have been over-inflated by VC funding.

Examining specific company performance since 2022 reveals a clear trend: the largest fastest-growing companies are exclusively in the mental health sector. Conversely, companies that have experienced the most significant contractions are those primarily employing medical clinicians or operating in non-mental health fields.

In order to better understand these industry trends, we grouped companies by verticals and looked at their growth before and after 2022.

Mental Health, Physical Therapy, Radiology, and Metabolic Health are the four verticals that have grown since 2022. These four verticals appear to have different stories of growth.

Addiction, Primary Care, and Telehealth Staffing are all somewhat down since 2022. The shared story among these verticals is over-hiring during the VC boom times. After the initial pandemic surge, demand didn’t grow as fast as hoped, which led to some retraction. In these verticals, demand for telemedicine has not reduced, it just hasn’t grown as fast as hoped.

The category of companies that had significant business in online ADHD treatment, led by Cerebral, done., and Ahead, have experienced major retraction since 2022. Much has been reported about the troubles of these companies. Even after the retraction, our data shows Cerebral is still the largest employer of nurse practitioners, and the third largest employer of all clinicians within the telemedicine industry.

Now that we have a few years of growth data across many telemedicine companies, we can compare the relative growth of employment models and distribution strategies.

Most telemedicine companies follow an employment model hiring their clinicians as employees. More recently a handful of MSO or “business in a box” telemedicine companies have grown. The MSO companies usually contract with clinicians on a 1099 basis. These companies have been concentrated within mental health and include Headway, Alma, Sondermind, Grow Therapy, and Rula. To compare the models, we can look specifically at the mental health vertical.

Since 2022 both categories have grown, but MSO models have grown much faster increasing +132% in size. The MSO model has economic advantages for the company: clinicians bear the risk of their time being unutilized, and, in many cases, marketing is left up to the clinician. These are big advantages that allow MSO companies to scale faster.

There are two primary ways for telemedicine companies to acquire new patients. The first is direct-to-consumer (DTC), in which they can market directly to them via consumer channels like Google, Meta, and Tiktok. The second is B2B2C, where the healthcare company gets access to non-public distribution channels via employers, payers, or other providers. So, which approach has shown enduring growth? Across all verticals DTC companies have shown +18% since 2022 while B2B2C has seen +39% growth. We can look specifically at Mental Health and Metabolic Health, which are two verticals with large amounts of both DTC and B2B2C companies.

Mental Health shows high growth in both models. This is driven by the set of mental health MSO companies which have been able to get wide payer coverage and acquire patients through broad DTC channels in addition to employer and health plan channels.

On the other hand, Metabolic Health shows stronger growth in B2B2C. B2B2C companies like Virta and Omada have shown consistent growth, while weight loss and GLP-1 focused DTC companies have been more boom and bust.

2020-2022 was a period of high scale experimentation fueled by venture funding in healthcare to understand what verticals and models were the best fits for telemedicine. Some experiments ended very poorly, some just ended, and others have emerged with sustained growth. After reviewing the growth of hundreds of telemedicine companies, let’s step back and synthesize some learnings.

Is telemedicine dying? Clearly not. Is telemedicine thriving? We would say so, though some verticals are still recovering from being given too much venture money. New wave telemedicine companies look more integrated into in-person care either by carving out remote jobs that fit into care teams or introducing technology that provides a novel "at-home" treatment experience. Standalone telemedicine services have shown to be an edge case in all of healthcare, so this is a natural evolution.

The telemedicine wave of 2020-2022 gave us answers to where telemedicine has enduring fit, but otherwise healthcare remains a primarily in-person and local industry. Our hope is the telemedicine wave, while not as immediately impactful as hoped, created a cohort of clinicians and operators game to build a next generation of healthcare services, likely grounded in in-person care, augmented by telemedicine, and utilizing efficiencies from technology wherever possible to provide better experiences for patients.

To inform this report, we analyzed the LinkedIn work history of 115,077 clinicians who have ever worked at a “telemedicine company”. Telemedicine Companies were defined as companies that employed at least 2 clinicians at some point between 2016 and 2024 and where the majority of those clinicians reported their jobs were fully remote.

There are limitations to this analysis. First, many clinicians don’t have LinkedIn profiles. Second, we only had access to public LinkedIn profiles. This means our numbers are an underestimate of the number of clinicians in the telemedicine workforce. The absolute numbers are not correct, but we believe since these limitations apply to all companies, comparisons across companies and across verticals should be accurate enough to extract insights.

Fair Use: Feel free to use this data and research with proper attribution linking to this study.

Media Inquiries: For media inquiries, contact team@singleaimhealth.com

Thanks to George Ribaroff, Kusum Chanrai, Tyler Olkowski, Lindsey Conon, Michael Ceballos, Jean Kim, Eddie Czech, Arpan Parikh, and Patrick Hurley for reviewing this article.

Chris, founded Single Aim Health in 2024 to provide clinicians, especially NPs and PAs, with essential services for launching and growing their practices. A Stanford graduate in Product Design, Chris co-founded Momentus Media, which was acquired by Facebook, and worked as a Product Manager there. He later gained expertise in digital health through leadership roles at Bicycle Health, Virta Health, and founding Wink Health. Now, he is using his experience to help clinicians through Single Aim Health.